This blog explores how HMRC’s anticipated introduction of joint and several liability (JSL) may arise in the labour supply chain and the extent to which liability may attach to the parties operating within it.

The analysis focuses on where the liability rests and HMRC’s powers of recovery against the individual entities under three types of engagement.

What is Joint and Several Liability?

- HMRC has published guidance at EMS2420 citing the introduction of new legislation at Section 61Y Chapter 11 of Part 2, ITEPA 2003, which is expected to come into force on 6th April 2026.

- The guidance explains the circumstances in which the employment business (Agency or Neutral Vendor) can become jointly and severally liable for tax and national insurance contributions when in a contractual chain with an umbrella company.

- Both the umbrella and the relevant party will be liable to pay any amount payable, in relation to any qualifying umbrella company payment, in accordance with the PAYE Regulations found at Chapter 11, Part 2 of ITEPA 2003.

- For the avoidance of doubt, the new legislation operates on a strict liability basis and so evidence of mitigation and due diligence will not offer any defence against JSL. Where the qualifying umbrella payment is not paid to HMRC, they can seek recovery from both the umbrella and the relevant party in the supply chain.

- Equally, HMRC’s guidance states that it does not matter which party pays or how much each party pays as long as the amount is paid in full.

Initial entity guidance from HMRC

HMRC’s guidance offers some initial indications of who the relevant parties are for the purposes of JSL;

Umbrella company contracts directly with the client

Where the client contracts directly with the umbrella company, the client will be the relevant party, and the liability will be joint and several between the umbrella company and client.

More than one intermediary in the contractual chain

If there is one or more intermediaries contractually interposed in the supply chain between the umbrella company and the client, the agency in the supply chain who has a contract with the client to supply the worker will be joint and severally liable with the umbrella company.

If the intermediaries in the chain are connected

If the agency and the client are connected the measure will apply as normal. The agency that contracts with the client will be jointly and severally liable alongside the umbrella company.

If the agency that contracts with the end client and the umbrella company are connected, then the client will be jointly and severally liable alongside the umbrella company and the agency.

If the client and the umbrella company are connected, then the measure will apply as normal. If there are one or more agencies in the contractual chain, then the agency that holds a contract with the end client will be jointly and severally liable alongside the umbrella company. If there is no agency in the labour supply chain, the client and umbrella company will be jointly and severally liable.

A company is connected with another company if:

- the same person has control of both

- a person has control of one and persons connected with him, or he and persons connected with him have control of the other

- a group of two or more persons has control of each company, and the groups either consist of the same persons or could be regarded as consisting of the same persons by treating (in one or more cases) a member of either group as replaced by a person with whom he is connected.

A company is connected with another person if:

- the same person has control of it

- or if that person and persons connected with him together have control of it.

Any two or more persons acting together to secure or exercise control of a company shall be treated in relation to that company as connected with one another, and with any person acting on the directions of any of them to secure or exercise control of the company.

Overseas intermediaries

If a worker is placed with a UK client by or through a non-UK resident agency, then the client is jointly and severally liable alongside the umbrella company.

Where the agency and employer they contract with are non-UK resident and there are other parties in the chain, the UK agency closest to the client is jointly and severally liable alongside the client.

The different scenarios- Analysis

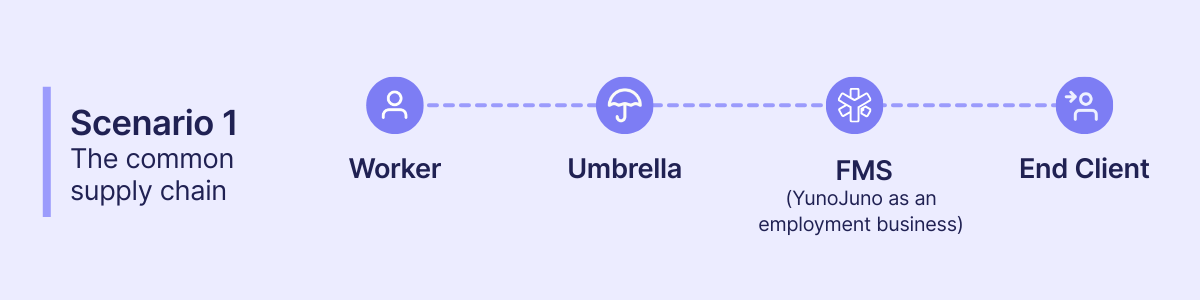

Scenario 1 - The common supply chain - Worker – Umbrella – FMS (YunoJuno) – End Client

- Here the JSL liability will sit with the umbrella who employs the worker and the neutral vendor (FMS) who has the contract with the End-Client. The End-Client is not impacted under JSL.

- The PAYE reference used to make the payments will be the Umbrellas.

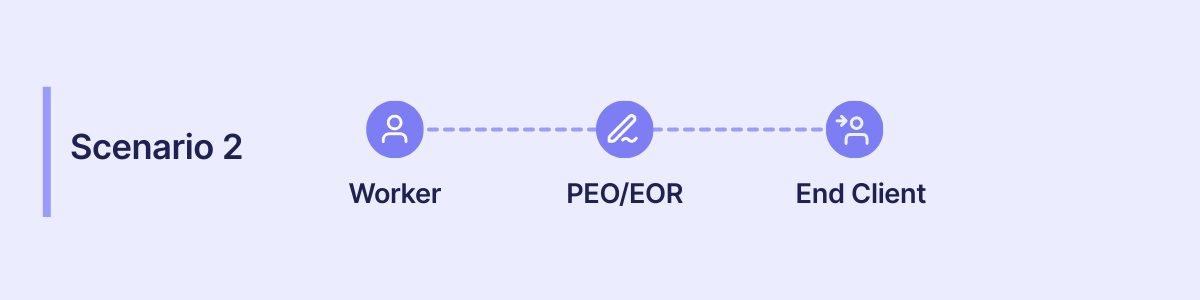

Scenario 2- Worker – PEO/ EoR – End Client

- Here the PEO (Professional Employer organisation) or EoR (Employer of Record) will employ the worker directly and payrolling will take place at this level.

- The PAYE reference used will be that of the PEO/ EoR and for the purposes of the legislation the JSL responsibility will be on both the End-Client and the PEO/ EoR because the PEO/ EoR will be determined as a purported umbrella.

Scenario 3 – Worker – End Client

- Here the end client would be managing PAYE as an employer and so JSL would not apply. The normal routes for recovery against the end client as the employer would apply under the PAYE Regulations.

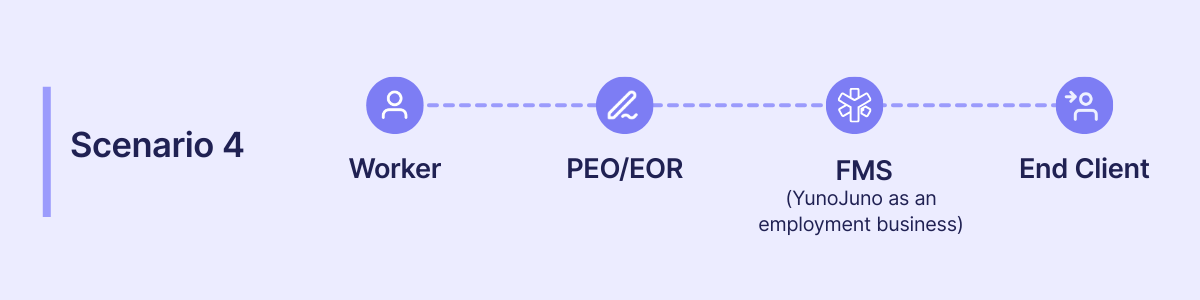

Scenario 4 – Worker – PEO/ EoR – FMS (YunoJuno) - End Client

- Here, the PEO/ EoR would engage the worker, however with the existence of a neutral vendor (FMS) in the supply chain, the end-client is protected from JSL and instead the liability would rest between the PEO/ EoR and the Neutral vendor.

- The PEO/EoR’s PAYE reference would be used to make the payment.

Mitigation Steps

- As explained above, this is a strict liability position and so due diligence and mitigation will not be a defence to the liability.

- The only way that the end client or Neutral Vendor in the above scenarios can mitigate liability is by knowing that tax has been paid by the umbrella and further protecting via available insurance products. Equally the end client can mitigate exposure by working with reputable and highly compliant Neutral Vendors in the supply chain.

YunoJuno’s Mandating of SafeRec certified umbrellas

- YunoJuno only engage SafeRec certified umbrellas in their supply chain.

- This is an effective mitigation tool for the end client because SafeRec independently verifies every month that the correct amount of tax has been physically paid to and received by HMRC, via a live check of the umbrella’s government gateway portal.

- All payslips are verified directly from the payroll organisation, not the umbrella and a subsequent report detailing all workers that have gone through the SafeRec process is issued to the Neutral Vendor such that they can further check that all workers are accounted for.

- Further, by selecting the three most financially viable umbrella organisations to work with, Yuno Juno further mitigates non-payment of PAYE through business failure.

- Finally, Yuno Juno will shortly be purchasing an insurance policy that will insure against the tax risk where the umbrella organisation fails to pay the tax liability, following a SafeRec audit. This further layer of protection, secures the supply chain from risk.

Conclusion

The JSL rules can create considerable risk in the supply chain for all entities. It is imperative that End Clients engage with reputable and highly compliant suppliers, such as YunoJuno, to ensure that tax risk is mitigated from being visited upon them. It is also equally important that agencies engage with appropriate transparency and mitigation tools such as SafeRec to ensure that contractual indemnities are not triggered, due to exposure inadvertently sitting with their clients.

Note: Our comments are based on the draft legislation contained within the Finance (No. 2) Bill as introduced to the House of Commons 4th December 2025.